AITAH for Telling My Ex-Wife to Get Her Own Insurance After Our Divorce Filing?

Divorce is not just about signing papers and moving on. Even after a couple separates, there can still be many shared responsibilities like finances, insurance, and other legal or financial matters that take time to sort out. This can make the process stressful and confusing for both people.

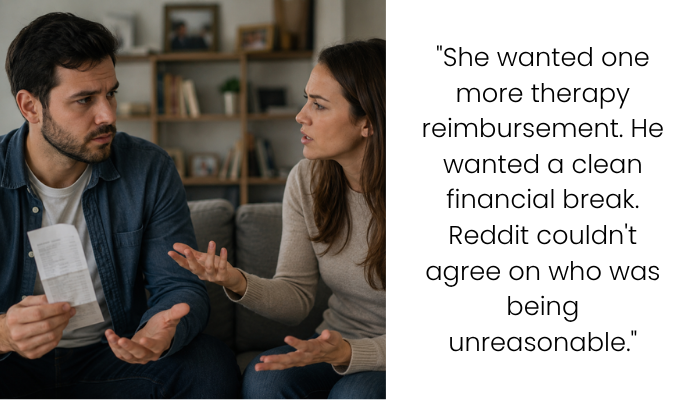

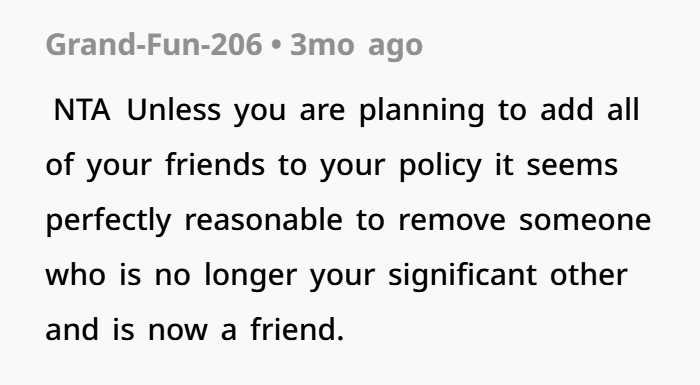

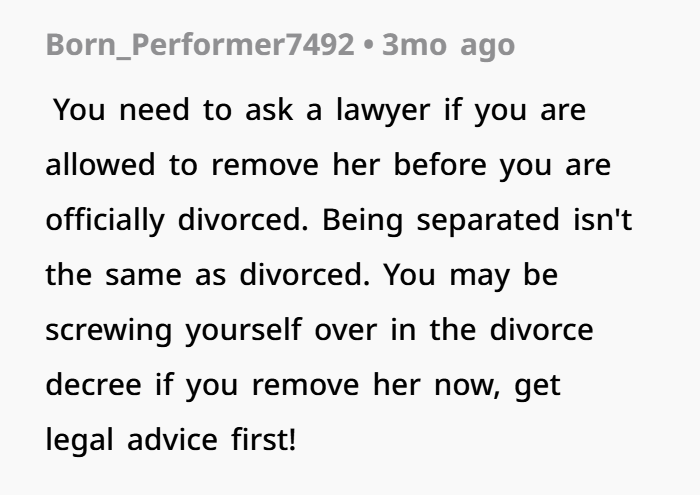

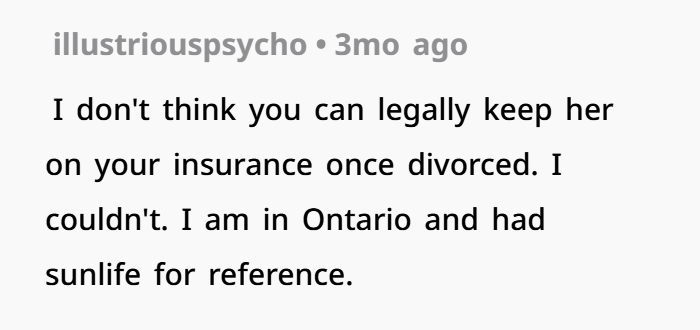

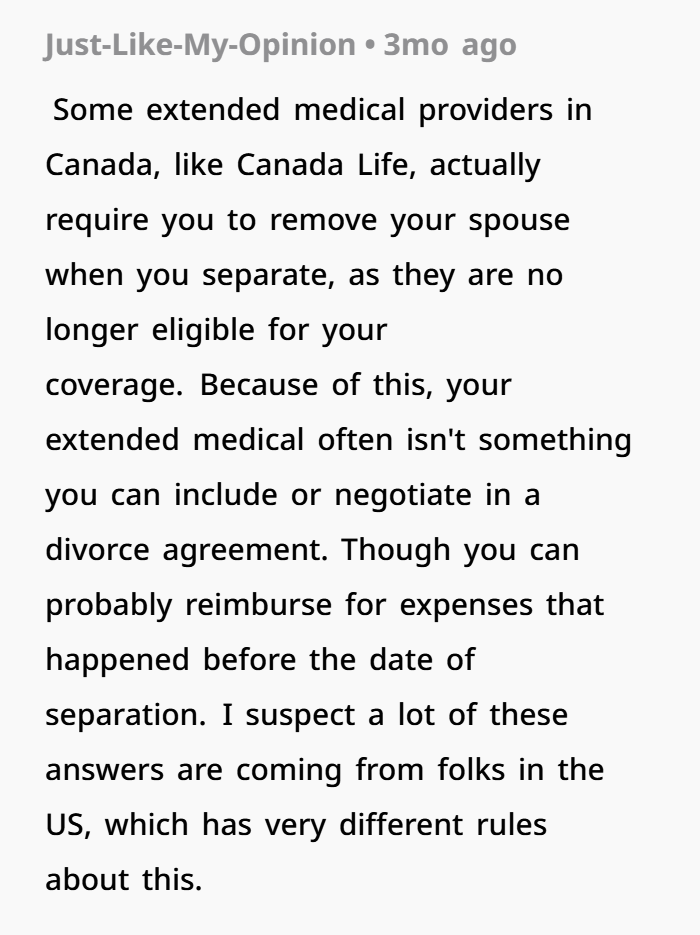

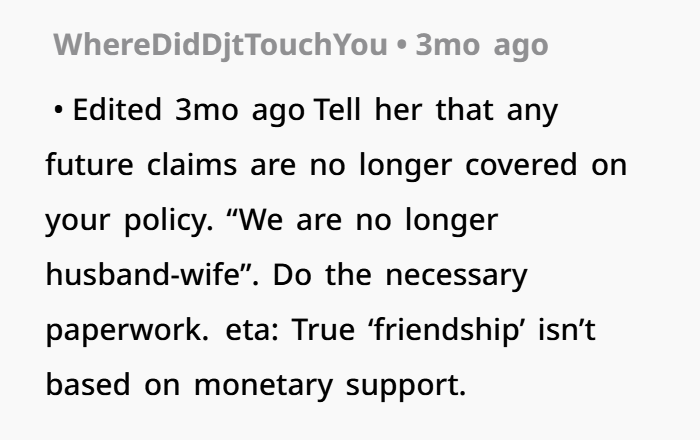

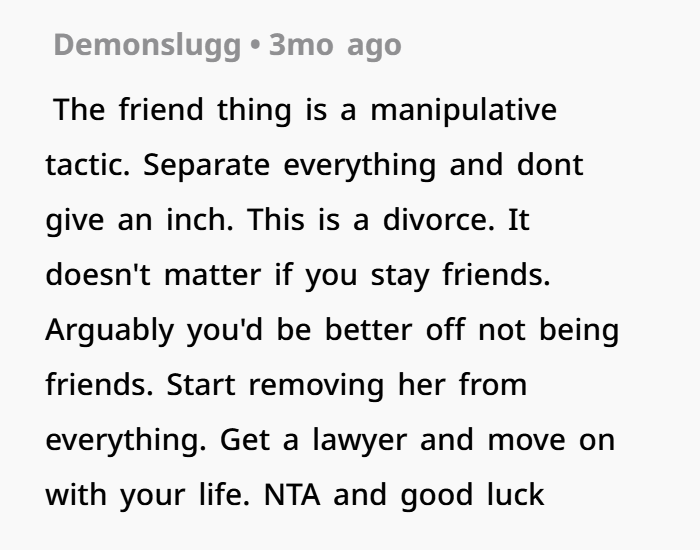

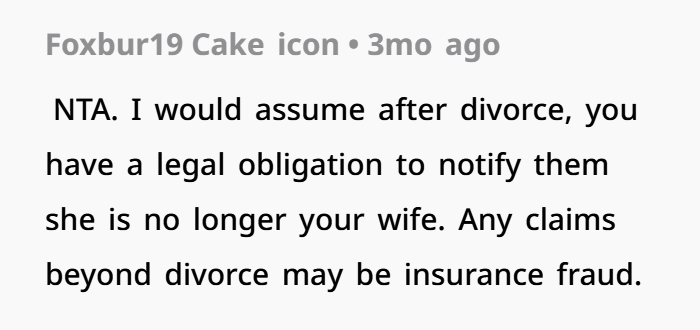

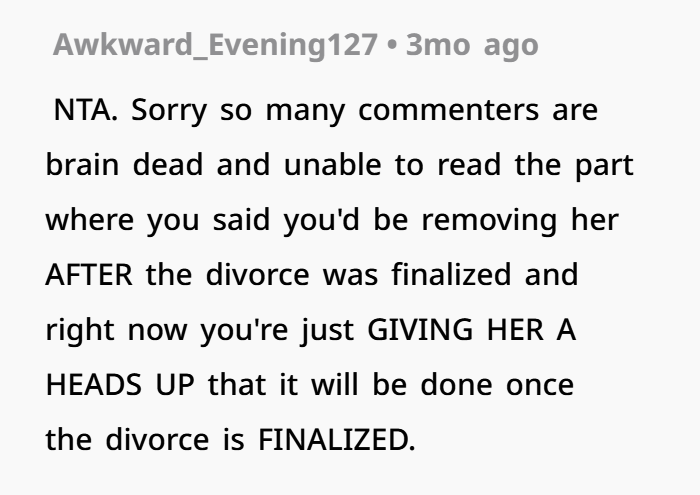

In this case, a man in Canada had been living separately from his wife for over a year and was in the middle of finalizing their divorce. During this time, his ex-wife asked him to submit another therapy reimbursement claim through his workplace health insurance. He agreed to help with the current claim, but he also told her that she should start arranging her own health insurance coverage because he planned to remove her from his policy once the divorce was completed.

His ex-wife did not react well to this conversation. She became upset and questioned whether he still wanted to stay friendly after the separation. The situation created tension between them, especially around financial planning, insurance coverage, and post-divorce boundaries.

Now he is unsure if setting this kind of financial and legal boundary was the right decision or if it came across as too harsh. This situation shows how important clear communication, financial independence, and legal planning are during divorce, especially when it comes to health insurance, shared benefits, and moving forward after separation.

Simple Explanation of a Workplace Conflict (Easy English)

This story is about a common problem in many corporate jobs, office environments, and government workplaces. It is not about a big argument or bad behavior. It is about how work expectations slowly change over time.

It also shows issues like employee burnout, HR management problems, workplace culture, and quiet quitting.

Doing the Job vs Doing Extra Work

The employee in this situation was still doing their normal job properly.

They:

- Completed their daily tasks

- Met their work goals

- Stayed productive at work

- Followed office rules

So there was no problem with their main job performance.

But the issue was something else.

They stopped doing extra unpaid work that was not part of their official job role.

Extra Work That Became “Expected”

In many workplaces, some employees do extra tasks without extra pay. This is common in workplace culture and employee engagement.

This employee used to do a lot of extra things like:

- Planning office events

- Organizing birthdays and celebrations

- Helping with team activities

- Improving office morale

- Supporting coworkers emotionally

At first, this extra effort was appreciated.

But slowly, it started to feel like it was “required,” even though it was not in the job description.

This is a common issue in many HR management systems.

Misunderstanding at Work

The situation became more serious after a private conversation between coworkers.

The employee tried to help a coworker understand a workplace policy update. This is normal in many offices. Employees often talk about:

- Work changes

- Stress at work

- Company policies

- Daily job problems

But management only saw part of the conversation.

Because of that, they misunderstood the employee’s intention and thought it showed a negative attitude.

This is a common problem in workplace communication and leadership management when full context is not understood.

Performance Review Problems

Later, the employee received a lower performance review.

This was surprising because their actual work was still strong.

But the review focused on things like:

- Attitude at work

- Team participation

- Office involvement

- Workplace behavior

These are subjective areas in performance review systems, and different managers may see them differently.

This made the employee feel confused and upset because their work performance had not changed.

Burnout and Work Stress

Over time, the employee started feeling tired and stressed.

This is called employee burnout, and it is very common in modern workplaces.

Burnout can happen when:

- Workload is too high

- Extra work is not appreciated

- There is no proper rest time

- Stress builds up over months or years

The employee explained that they needed a better work-life balance and could not continue doing extra unpaid work.

These are normal concerns in today’s corporate work culture.

What “Quiet Quitting” Means

After this, the employee changed how they worked.

They did NOT quit their job.

They did NOT stop working.

They did NOT refuse their duties.

Instead, they simply stopped doing extra tasks outside their job role.

This is called quiet quitting in the workplace.

Quiet quitting means:

- Doing only the work you are paid for

- Not taking extra unpaid responsibilities

- Setting healthy boundaries

- Protecting mental health and energy

This trend is becoming more common in modern office jobs and corporate environments.

Office Events and Responsibility Issues

Later, there was an office event that needed planning.

The employee clearly said in advance that they would not organize it.

But when the event date came closer, there was confusion about who should handle it.

This showed a bigger issue in the workplace:

When tasks are not clearly assigned, companies often rely on one person’s extra effort.

This is a workplace management and HR planning problem, not just an employee issue.

Growing Workplace Tension

After this, management raised concerns about:

- Team participation

- Office engagement

- Attitude in workplace activities

Even small things, like not fully participating in office events, were mentioned.

This created more tension between the employee and management.

In many companies, when employees feel forced to participate in everything, employee engagement and job satisfaction can go down.

Why Employees Step Back

The employee explained they were feeling burned out and needed rest.

This is very common in workplace stress and employee well-being discussions today.

Employees often step back from extra work when:

- They feel overworked

- Extra effort is not recognized

- Mental health is affected

- There is no proper work-life balance

This is not rebellion. It is self-protection.

The Bigger Lesson for Workplaces

This situation shows a bigger issue in many companies:

- Extra work is often not clearly defined

- Some employees carry too much responsibility

- Emotional labor is not always rewarded

- Communication between staff and management is weak

Over time, this can damage workplace culture, employee retention, and job satisfaction.

What The Comments Reveal

Final Thoughts

This story is not about one employee refusing to work.

It is about how workplace expectations can slowly change.

The employee was still doing their job. They only stopped doing extra unpaid work.

This small change created conflict because the workplace had started depending on that extra effort.

It is a reminder for many companies to focus on:

- Fair workload distribution

- Clear job roles

- Strong HR management

- Healthy employee engagement

- Better work-life balance

When employees feel respected and supported, they are more likely to stay motivated and productive in the long run.