When My Husband Won’t Make Me a Beneficiary, I Made a Tough Choice

Money planning in blended families can be complicated, even when everyone is trying to do the right thing. In this case, a woman had been married for a little over a year. She had two adult daughters from a previous marriage. She was surprised when she learned that her husband did not want to name her as a beneficiary on his life insurance policy. This made her feel worried about financial security and future protection.

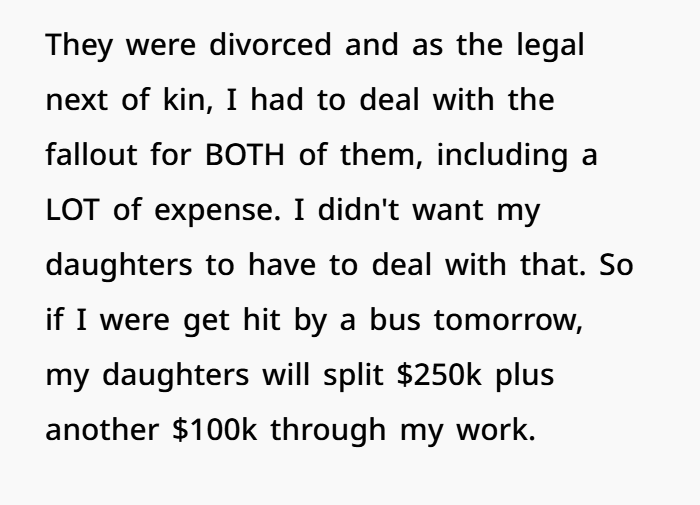

She had already experienced loss in her life, including losing both of her parents in her 30s. Because of that, she understood how hard it can be when there is no clear plan for life insurance, estate planning, or inheritance planning. To protect her own family, she made sure her life insurance and financial accounts were set up so that her husband and children would both be taken care of if something happened to her. She was trying to focus on long-term financial planning, retirement planning, and family financial security.

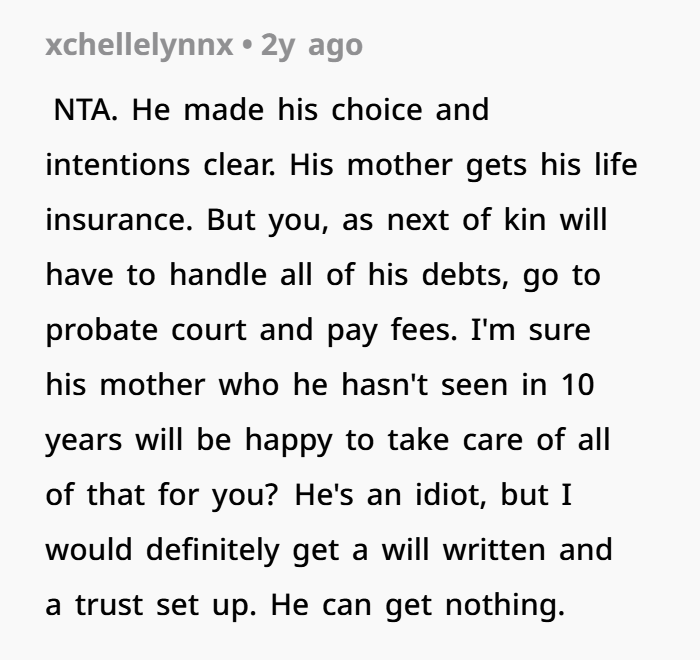

However, when she asked her husband to do the same for her and her children, he refused. He kept his mother as the only beneficiary, even though they were not close anymore. This made the wife feel unsafe and unprotected in the marriage. In response, she changed her own plans. She canceled his life insurance coverage and updated her beneficiary designations so that her daughters would receive her assets instead.

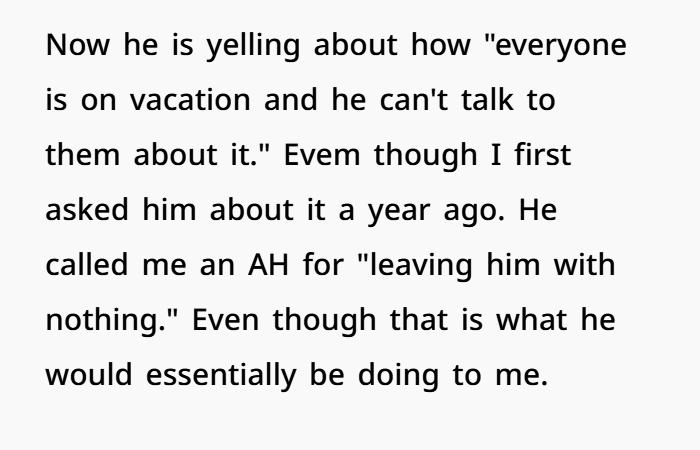

Now their relationship is under stress. Her husband feels hurt and says she left him without support. This situation shows how important open communication is in blended family financial planning, life insurance policies, and estate planning decisions. Without clear agreements, issues around beneficiaries, inheritance, and wealth protection can quickly create tension between spouses.

At first glance, this situation looks like a normal disagreement between a husband and wife. But when you look closer, it is really about financial planning, life insurance decisions, estate planning, and long-term financial security inside a blended family.

In simple terms, it shows how important it is for married couples to agree on money protection and beneficiary choices.

A Woman Focused on Financial Security

The wife in this situation has gone through a lot in life. She lost both of her parents in her 30s. Because of that, she had to deal with estate planning, bills, and financial responsibilities on her own.

This experience changed how she thinks about money.

She started focusing on life insurance coverage and long-term financial planning so her children would never face the same stress. She made sure her adult daughters would be financially protected if anything happened to her.

This is actually a smart move in personal finance. Many financial advisors say life insurance is an important safety net, especially for people with children or dependents.

Life Insurance for Her Husband

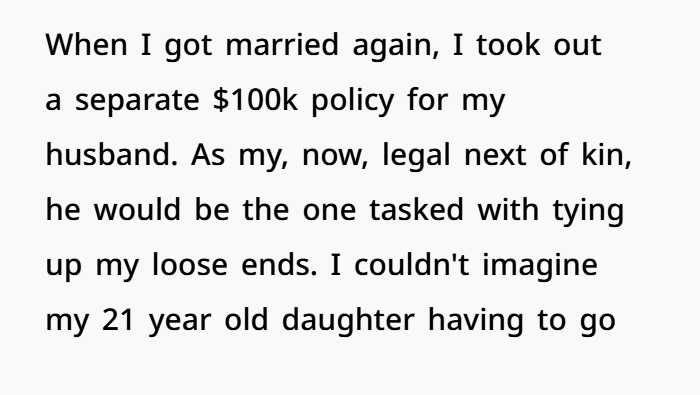

After she remarried, she also made a responsible decision for her new husband. She took a life insurance policy of around $100,000 for him.

The goal was simple: if something happened to her, her husband would not struggle with expenses or sudden financial problems. The amount was set in a balanced way based on income and needs.

This is common in retirement planning and insurance planning, where couples try to protect each other financially without causing extra burden.

So far, everything looked fair and thoughtful.

The Problem With Beneficiary Designation

The issue started when she asked her husband to list her as a beneficiary on his work life insurance policy.

A beneficiary is the person who receives the insurance money after someone passes away. It is a very important part of estate planning and wealth management.

But the husband refused.

Instead, he kept his mother as the only beneficiary—even though she is financially well-off and not closely involved in their daily life.

From a financial planning point of view, this can be seen as risky in a marriage. Usually, spouses are listed as primary beneficiaries because they share responsibilities and expenses.

Why This Became a Trust Issue

In many marriages, especially blended families, financial transparency and trust are very important.

When one partner is fully protected and the other is not, it can create imbalance.

In this case:

- The wife was taking care of her husband financially.

- She also included her children in her financial plans.

- But the husband did not include her in his life insurance policy.

This created emotional stress and raised questions about fairness and trust in the relationship.

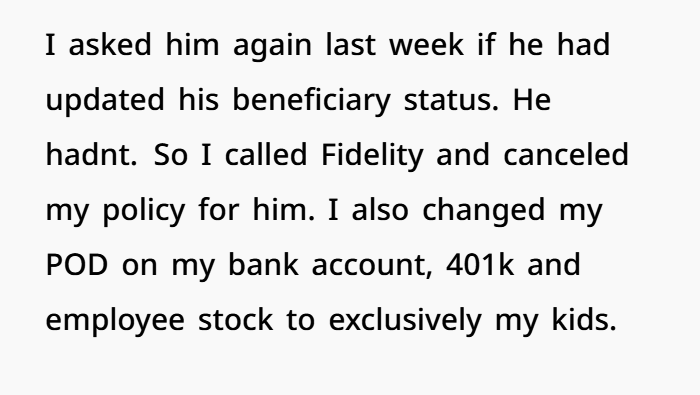

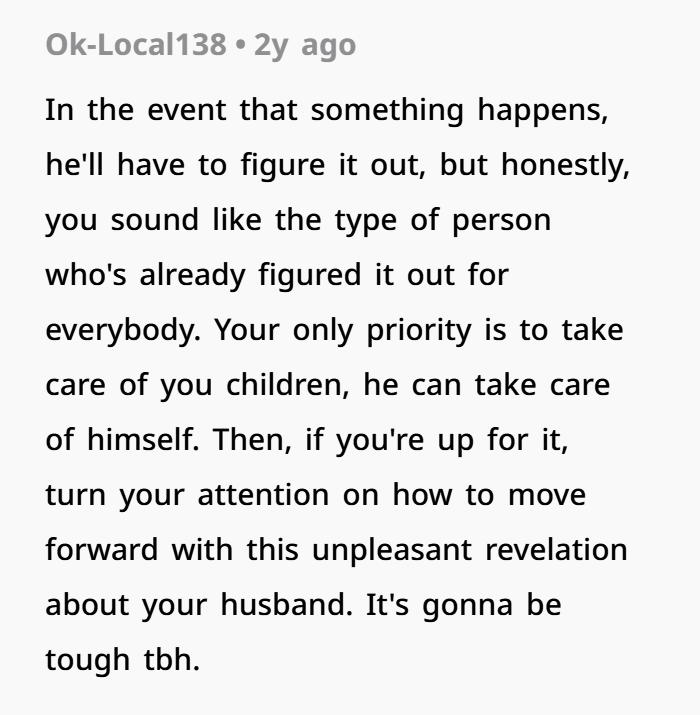

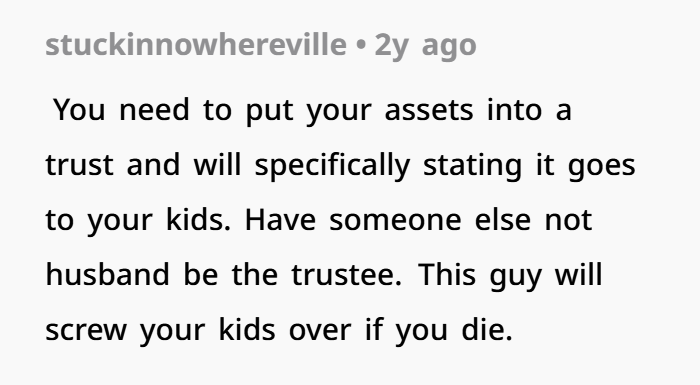

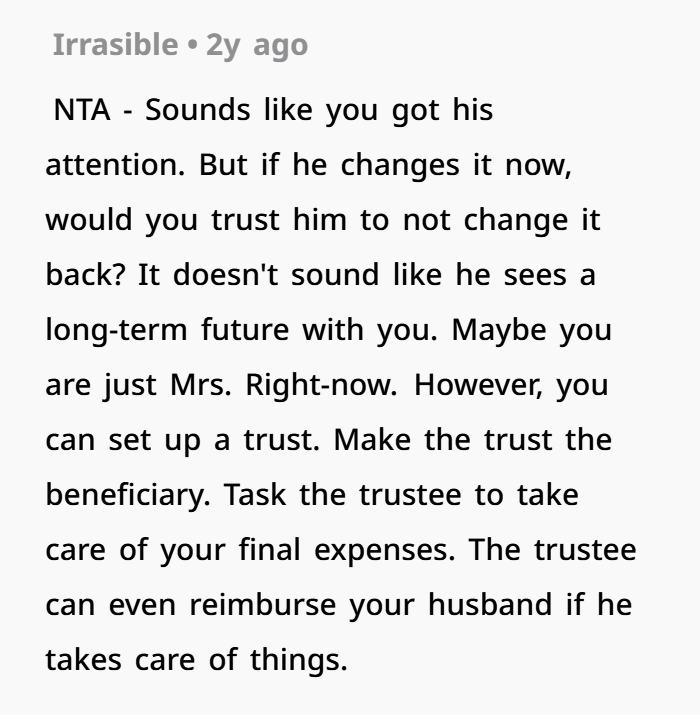

The Wife’s Decision to Cancel Coverage

After asking for a long time and getting no change, the wife decided to cancel the life insurance policy she had for her husband.

She also adjusted her own financial planning so that her assets and insurance would go directly to her children.

This is often seen in estate planning strategies, especially in blended families where each person wants to make sure their own children are protected.

From a financial security point of view, this is a way of reducing risk and making sure money goes where it is intended.

Blended Family Financial Planning Challenges

Blended families often face complicated money decisions. There are step-children, previous marriages, and different financial responsibilities.

That is why experts in personal finance and wealth management always recommend:

- Clear beneficiary designation

- Open communication about money

- Equal protection for both spouses

- Regular review of life insurance policies

Without these steps, misunderstandings can easily happen.

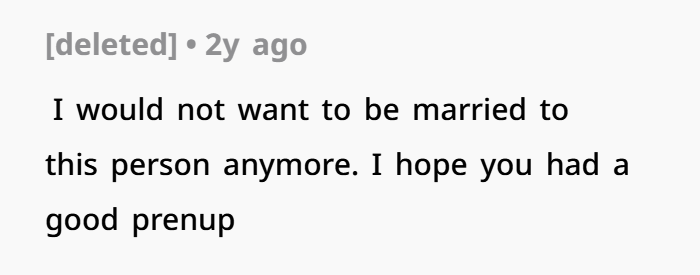

Was It a Fair Decision?

Some people may feel the wife’s actions were too strong. But from a financial planning perspective, her decision was based on logic, not emotion.

She:

- Tried to discuss it for a long time

- Wanted fair protection for both sides

- Took steps to secure her children’s future

- Focused on long-term financial stability

On the other hand, the husband did not change his beneficiary decision, which created imbalance in financial responsibility.

The Comments Are In

Final Thoughts on Financial Security in Marriage

This situation is not just about conflict. It is about life insurance planning, beneficiary decisions, estate planning, and financial protection in marriage.

In any relationship, especially blended families, both partners should feel financially secure and equally protected.

Money decisions may not seem emotional at first, but they play a very big role in trust and stability.

At the end of the day, financial planning is not just about money. It is about making sure both partners and children are safe, protected, and prepared for the future.

And that is what good financial security is really about.