AITA for Telling My Husband It’s Life Insurance or Divorce After His Family’s Cancer Diagnosis?

A successful 45-year-old business owner had a serious conversation with her husband about life insurance, disability insurance, and long-term financial planning. She became more aware of these issues after learning that her brother-in-law was diagnosed with pancreatic cancer and was advised to get genetic testing due to a strong family medical history. This made her think about how quickly medical emergencies can affect a family, both emotionally and financially.

She also remembered how her own mother struggled in the past while caring for a terminally ill partner. During that time, medical bills, loss of income, and caregiving stress created a lot of financial pressure. Because of these experiences, she strongly believes in financial security, asset protection, and having proper insurance coverage to avoid future debt. For her, this is an important part of responsible financial planning and retirement protection.

However, her husband did not take the conversation seriously. He laughed and joked that she could support him like a “sugar mama” and even said he would rather spend time gaming if he could not work due to illness or disability. His response made her feel worried and frustrated because she felt he was ignoring serious risks related to health insurance and disability coverage.

In response, she suggested something unusual: a legal divorce on paper while continuing the relationship in daily life. Her idea was not to end the marriage emotionally, but to protect her business assets, savings, and financial stability from possible future medical expenses or disability-related costs. Now she is unsure if she went too far or if her husband is not taking important financial risks seriously enough in their marriage and long-term financial planning.

At first glance, this story looks like a disagreement about life insurance, financial planning, disability insurance, estate planning, and long-term care planning. But the real issue goes much deeper than money.

It is really about fear, emotions, and how two people handle stress in very different ways.

Fear Behind Financial Planning

The wife is worried because of serious illness in her husband’s family. His brother has pancreatic cancer, and his father also died from the same disease. Because of this, doctors suggested genetic testing and closer health monitoring.

From her point of view, this is a serious warning sign. She has already seen what a long illness can do to a family. It can affect medical expenses, caregiving costs, emotional health, and financial stability.

She remembers how hard it was when her own family dealt with caregiving. She saw stress, financial pressure, and emotional burnout. Those experiences made her very focused on financial protection and future planning.

Why She Is Thinking About Insurance

The wife is not only thinking about death. She is thinking about what happens during illness, such as:

- Long hospital stays

- Cancer treatment and chemotherapy

- Nursing and caregiving needs

- Loss of income

- High medical bills

- Long-term care costs

This is why topics like life insurance, disability insurance, estate planning, and asset protection feel very important to her.

Financial advisors often say these are important conversations for couples, especially when there is a family history of serious illness.

Planning early can help protect savings and reduce stress during emergencies.

The Husband’s Different Reaction

The husband reacts in a very different way. Instead of showing concern, he seems calm or even joking about it.

Some people see this as not taking the situation seriously. Others think it may be a way of coping.

Many people use humor when they feel stressed or scared. It is a common emotional response. It does not always mean they do not care.

It is also possible that he is avoiding thinking about a future illness because it feels too uncomfortable.

Childhood Trauma and Emotional Response

There is also an important detail in the story. The husband had a difficult relationship with his father, who was reportedly abusive. After his father died, he felt relief instead of sadness.

This kind of past can affect how a person handles emotions later in life. People with childhood trauma may:

- Avoid emotional conversations

- Struggle with fear or stress

- Disconnect from difficult topics

- Focus on staying emotionally distant

Because of this, his reaction may not be about ignoring the problem. It may be about how he has learned to protect himself emotionally.

The Real Problem: Communication Gap

The biggest issue in this marriage is not insurance. It is communication and emotional understanding.

The wife is trying to prepare for risk. She wants security and reassurance that the family will be protected through financial risk management and estate planning.

The husband is trying to avoid fear. He does not want to think about worst-case scenarios or feel like illness is already expected.

So both people are actually speaking from fear, but in different ways.

What They Are Really Saying

The wife is really saying:

- “I don’t want us to lose everything if something happens.”

- “I want us to be financially prepared.”

- “I need security and peace of mind.”

- “I don’t want to face a caregiving crisis alone.”

The husband may be thinking:

- “I don’t want to live in fear of getting sick.”

- “I don’t want to assume the worst every day.”

- “I feel uncomfortable planning for something that may never happen.”

But neither of them is fully hearing the other side.

Why Insurance Became a Conflict

Instead of talking about feelings, the couple started arguing about insurance policies and financial decisions.

For the wife, insurance means safety and protection.

For the husband, insurance may feel like fear or pressure.

This is why the disagreement became stronger than expected.

The “Divorce” Comment

At one point, the wife mentioned divorce, but she was talking about it in a legal and financial protection sense, not ending the marriage emotionally.

Still, the word “divorce” can feel very heavy. It can sound like an ultimatum, even when that is not the intention.

This is where the conversation became more emotional and harder to manage.

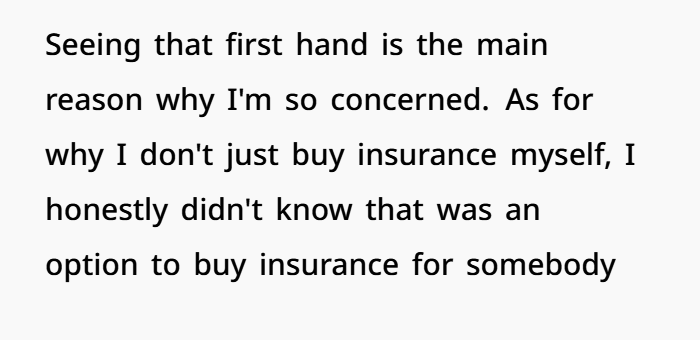

Finding a Better Way Forward

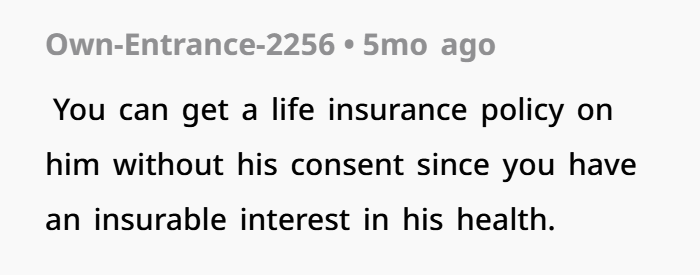

Later, the wife realized there may be other options, such as buying life insurance on a spouse with consent. This helped shift the situation toward a more practical solution.

This kind of planning is often used in family financial planning, wealth management, and estate planning strategies.

The goal is not to assume the worst, but to be prepared if something happens.

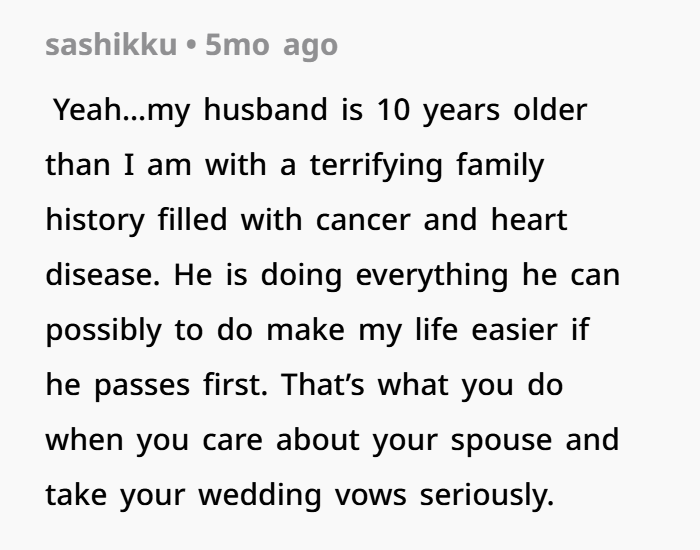

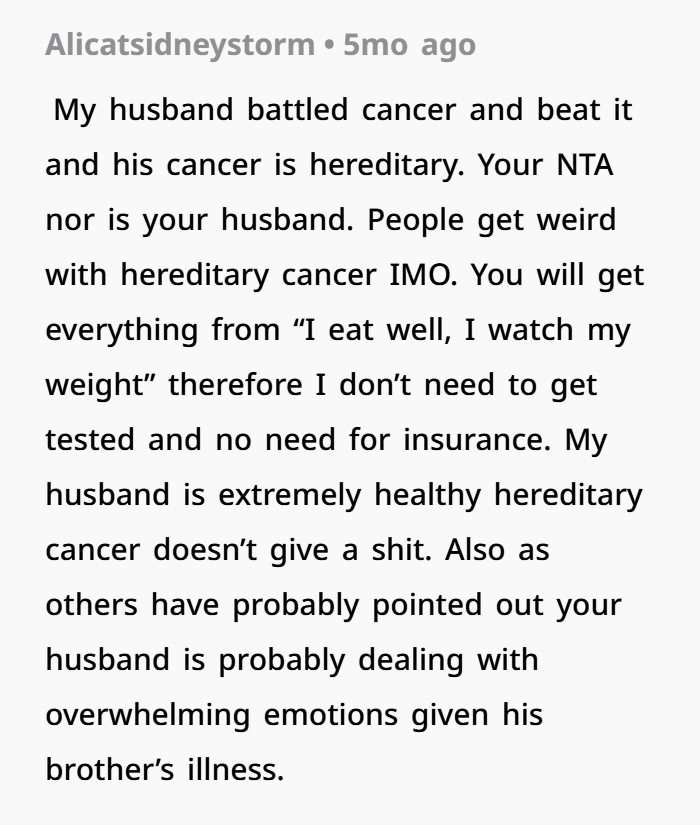

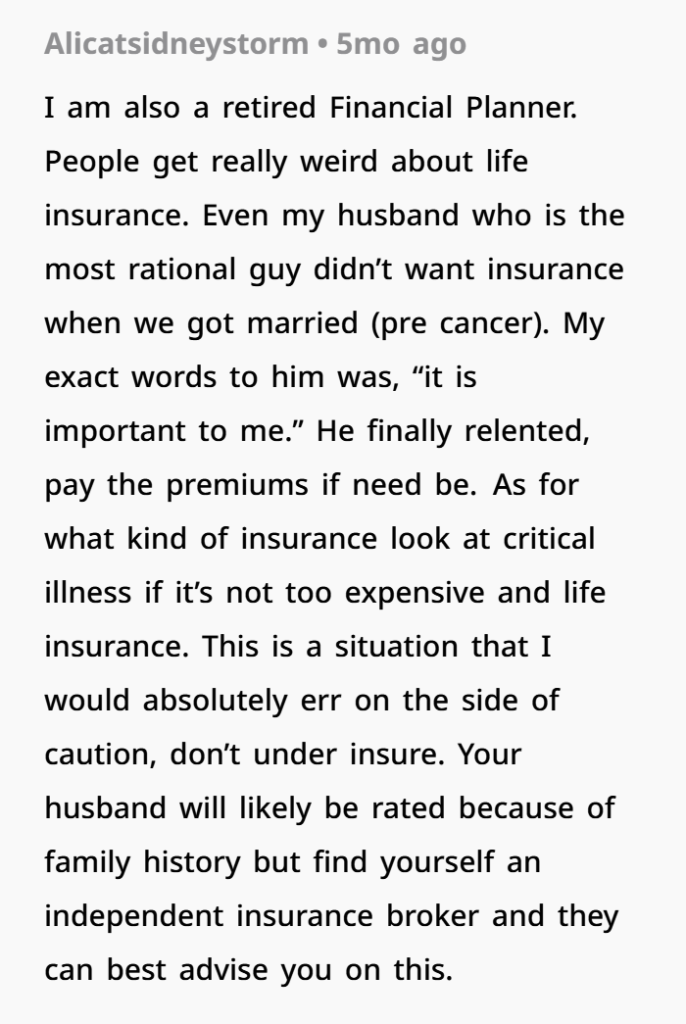

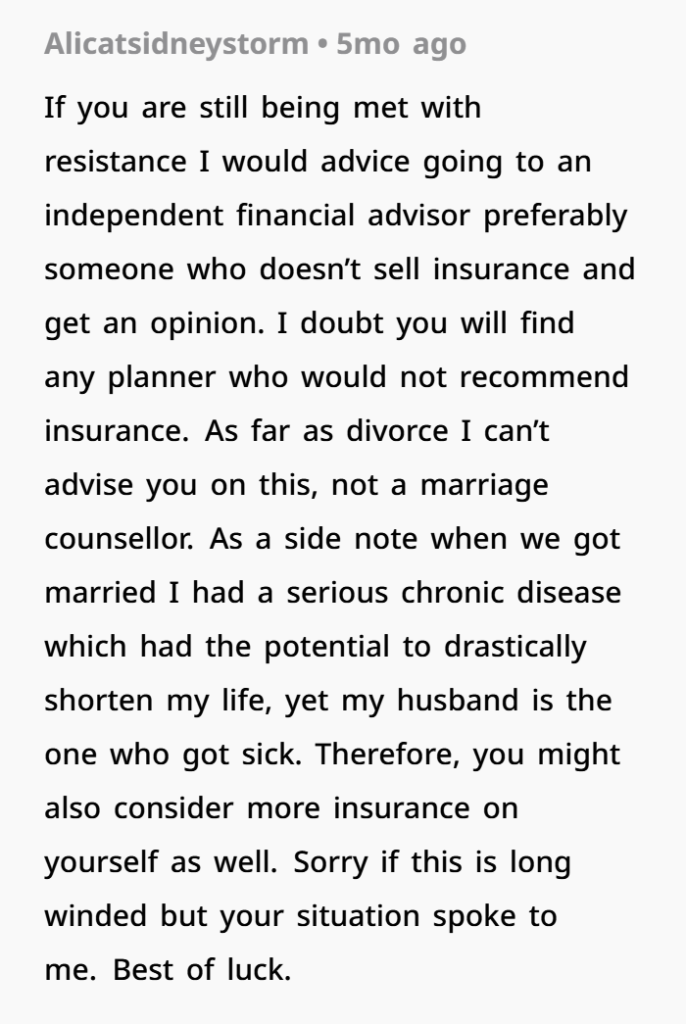

Top Comments From Readers

Final Thoughts

This story is not just about money or insurance. It is about two people reacting to fear in different ways.

The wife deals with fear through planning, preparation, and financial security.

The husband deals with fear through avoidance and emotional distance.

Neither approach is completely right or wrong.

The real solution is better communication, understanding, and balance between financial planning and emotional well-being.

In the end, strong relationships are not built on avoiding hard topics, but on facing them together with honesty and care.