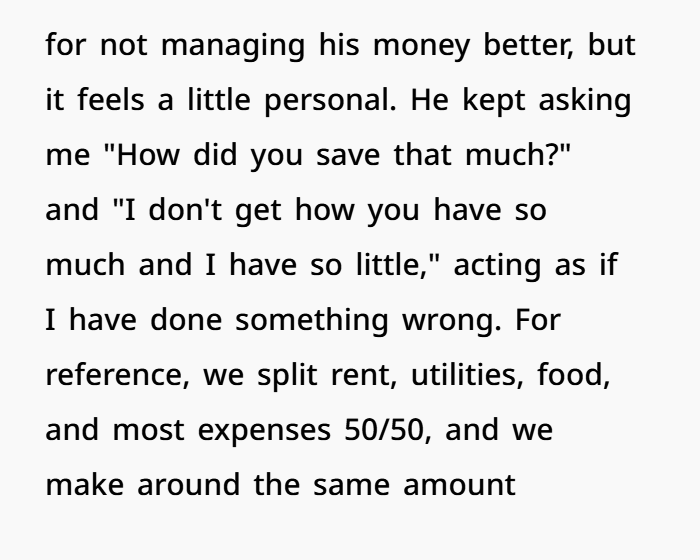

“My Boyfriend Cried When He Saw My Savings” — The Financial Reality Check That Changed Everything

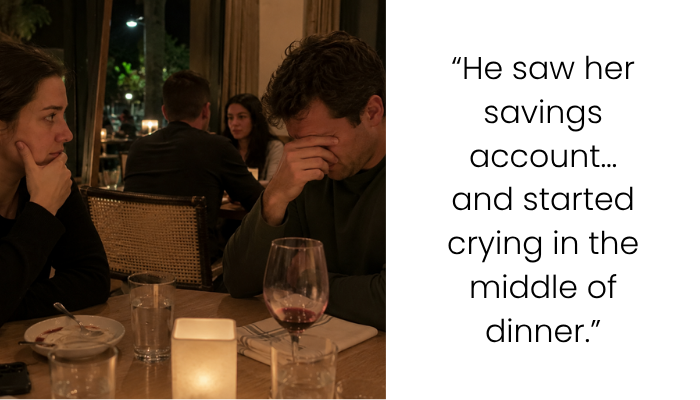

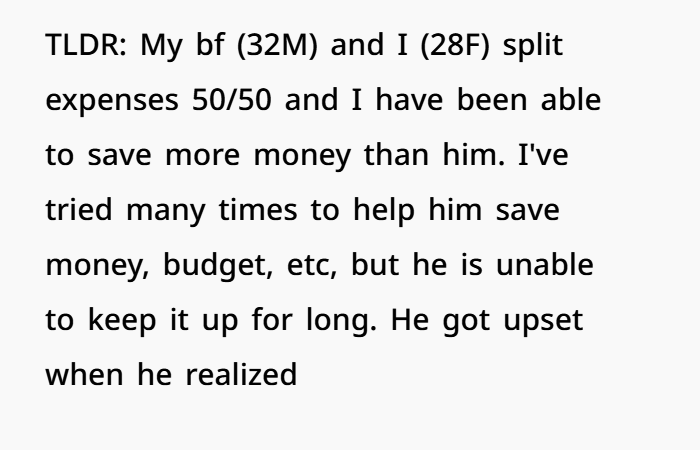

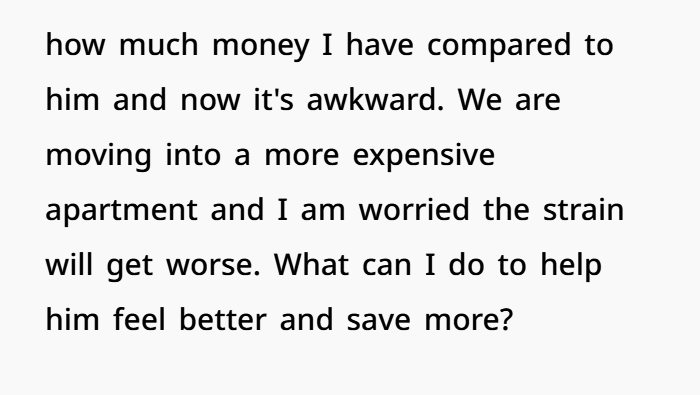

Financial issues can stay hidden in a relationship for a long time and then suddenly become a serious problem. In this case, a woman was talking with her boyfriend of seven years about moving into a more expensive apartment. During the conversation, she casually showed him her savings account while they were discussing their future living plans.

Instead of feeling positive about the future, her boyfriend became emotional and upset. He started crying, and the conversation about budgeting and rent quickly turned tense and uncomfortable for both of them.

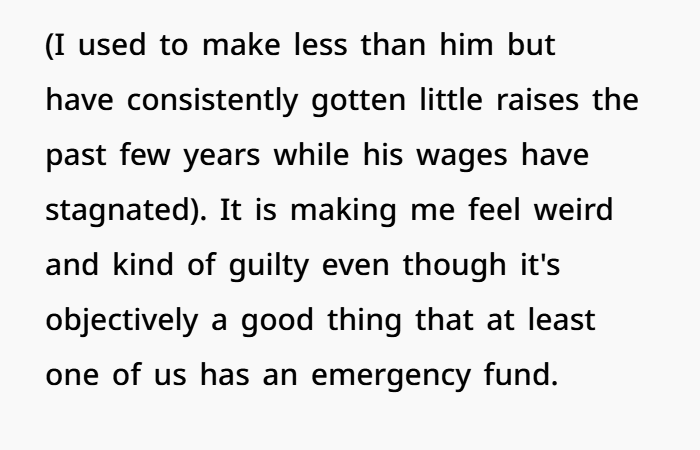

They usually split bills equally and earn similar incomes, but their spending habits are very different. The woman is careful with money, focused on saving, investing, and long-term financial planning. Her boyfriend struggles with impulsive spending and managing money consistently, which has made it harder for him to build savings.

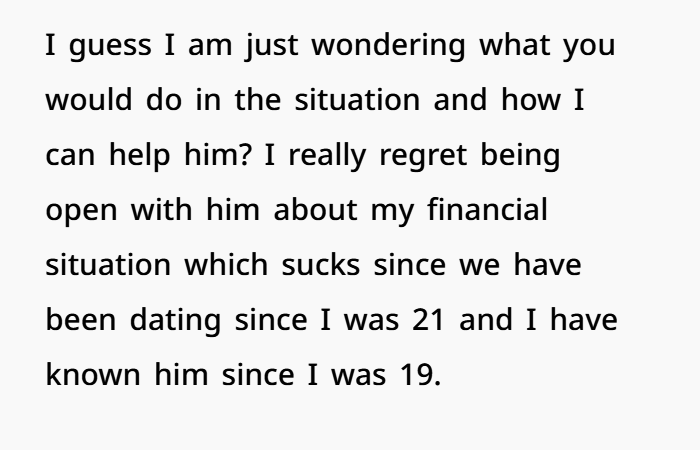

Seeing the difference in their finances made him realize how much he had struggled with money management over the years. This emotional moment created stress in the relationship, and the woman now feels unsure about how this financial gap could affect their future together, especially with higher rent, shared expenses, and long-term financial goals.

This situation highlights the importance of financial communication, budgeting habits, and financial compatibility in long-term relationships.

This story looks like a simple money problem at first, but it is actually much deeper. It is about emotions, financial stress, relationship pressure, and long-term compatibility between two people.

It Was Not Just About Money

The boyfriend’s emotional reaction was not only about how much money she had saved.

It was about what those savings meant.

Savings represent security, stability, and safety for the future. So when he realized his partner had built strong savings while he had very little, it created a strong emotional shock.

Same Income, Different Financial Results

The couple earned about the same salary and split expenses equally.

But their financial habits were very different.

Over time:

- She saved money consistently

- He struggled with saving

- Small spending habits added up

- Debt and fines started to build

This created a large financial gap between them.

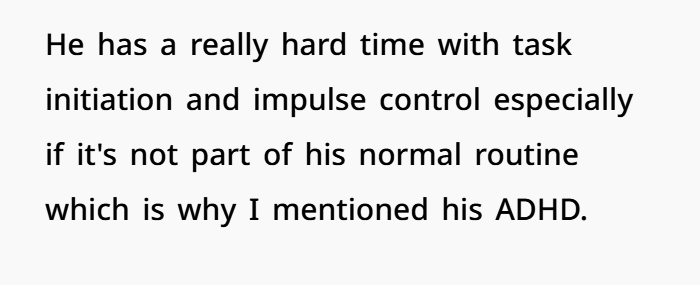

Financial Stress and ADHD Challenges

ADHD can make money management very difficult for some people.

Common struggles include:

- Impulse spending

- Poor planning

- Forgetting bills or fines

- Avoiding stressful tasks

- Difficulty saving long-term

These challenges can slowly create serious financial problems if not managed properly.

At the same time, these struggles do not remove responsibility, especially in a long-term relationship.

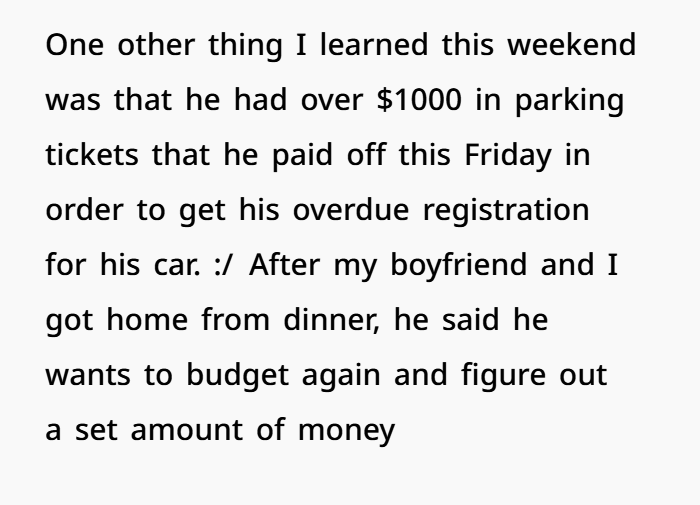

Hidden Financial Problems Build Over Time

In this story, unpaid parking tickets and car-related fines added up to over $1000.

This shows a pattern of avoiding small problems until they become big and expensive.

This kind of financial behavior can affect both partners in a relationship.

Why Financial Compatibility Matters

Financial compatibility is very important in long-term relationships.

Couples do not need equal income, but they do need:

- Similar money habits

- Shared financial goals

- Good budgeting skills

- Responsibility with spending

Without this balance, one partner can end up carrying most of the stress.

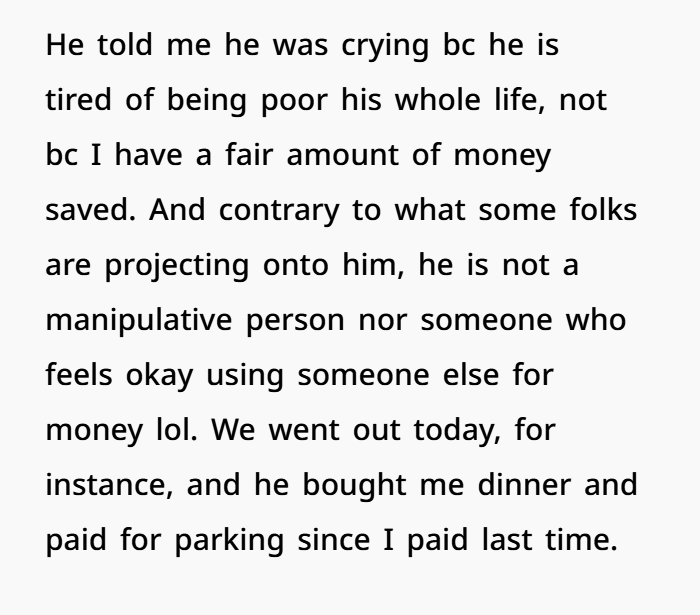

Emotional Reaction From Both Sides

The boyfriend felt shame and frustration when he realized the financial gap.

The girlfriend did not react with anger. Instead, she felt worried and guilty, even though she had done nothing wrong.

This shows she cares about his feelings and the relationship.

Pressure in Long-Term Relationships

Over time, one partner can start becoming the “manager” of the relationship finances.

This means they:

- Track bills

- Plan budgets

- Handle emergencies

- Give reminders

- Manage savings

This imbalance can become emotionally tiring.

Realization About the Future

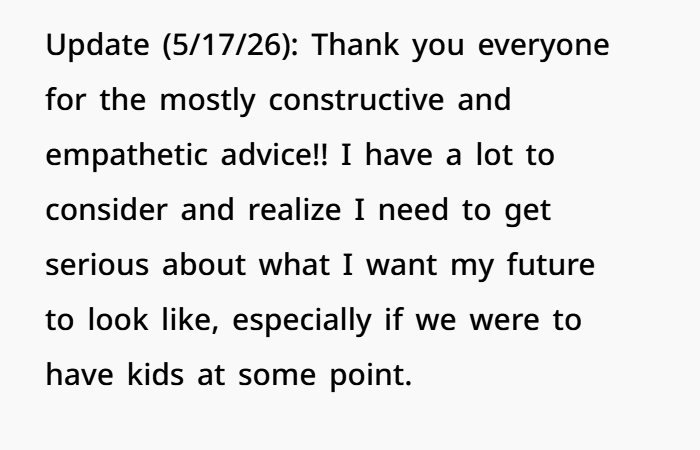

After seven years together, this moment became a serious wake-up call.

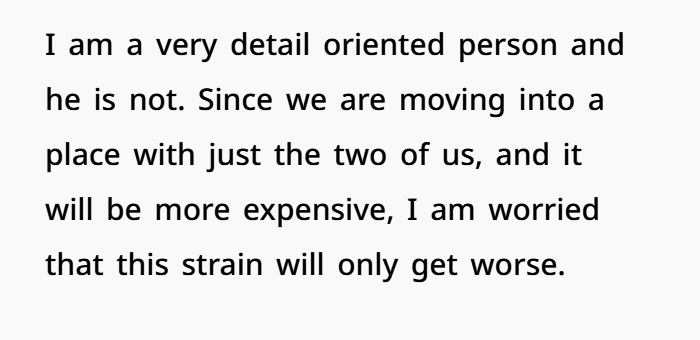

Moving into a more expensive home made the financial pressure even stronger. Rent, bills, and daily expenses become harder to manage when savings are low.

The Importance of Action, Not Emotion

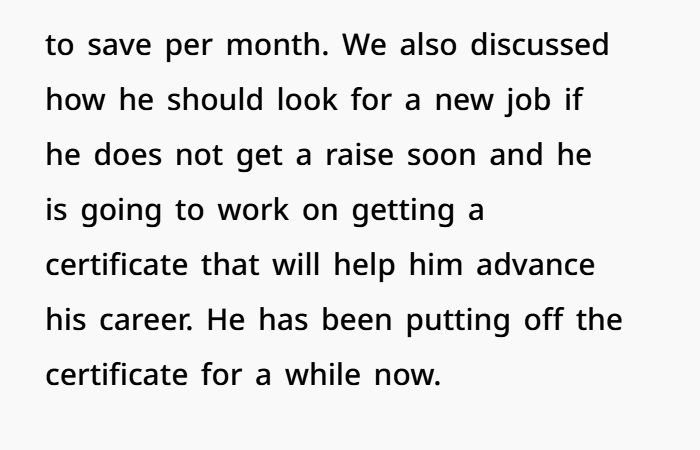

The boyfriend showed awareness of the problem and talked about:

- Better budgeting

- Career improvement

- Certifications

- Saving money

This is a positive step, but real change depends on consistent action, not emotional promises.

Why Consistency Matters

In financial stability, consistency is more important than motivation.

Helpful systems can include:

- Automatic savings

- Budget tracking apps

- Separate bill accounts

- Spending limits

- Therapy or coaching for ADHD

These tools can help build long-term financial stability.

Protecting Personal Financial Security

The girlfriend may also need to protect herself financially by:

- Keeping savings separate

- Avoiding shared debt for now

- Watching long-term behavior changes

- Not relying on promises alone

This helps reduce future financial risk.

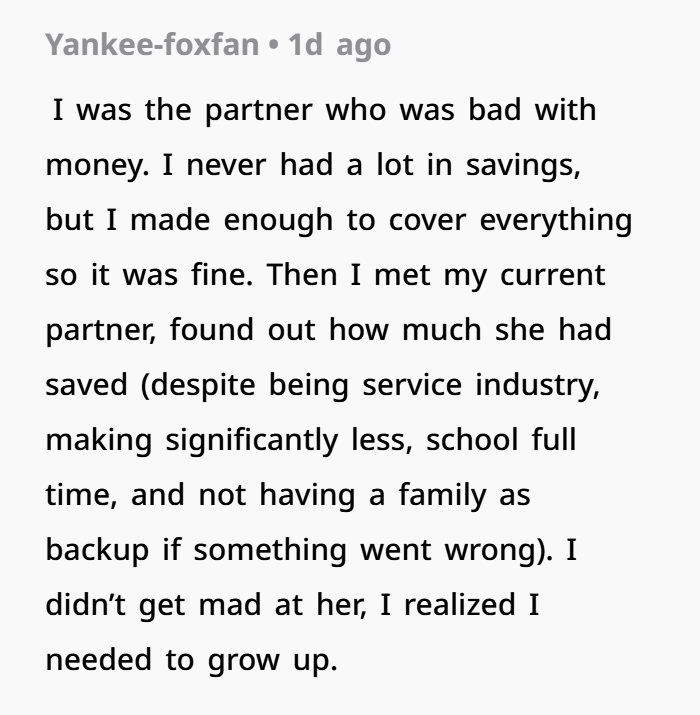

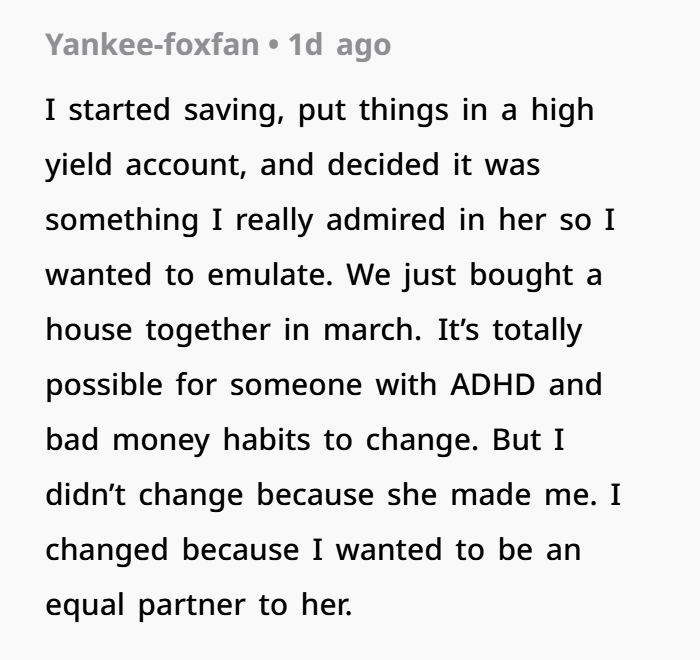

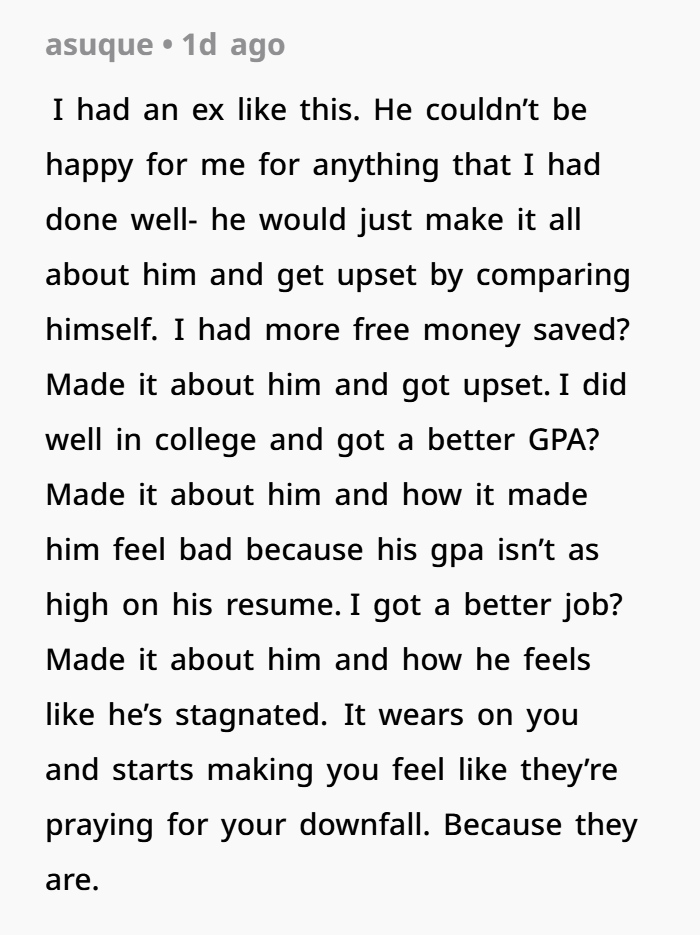

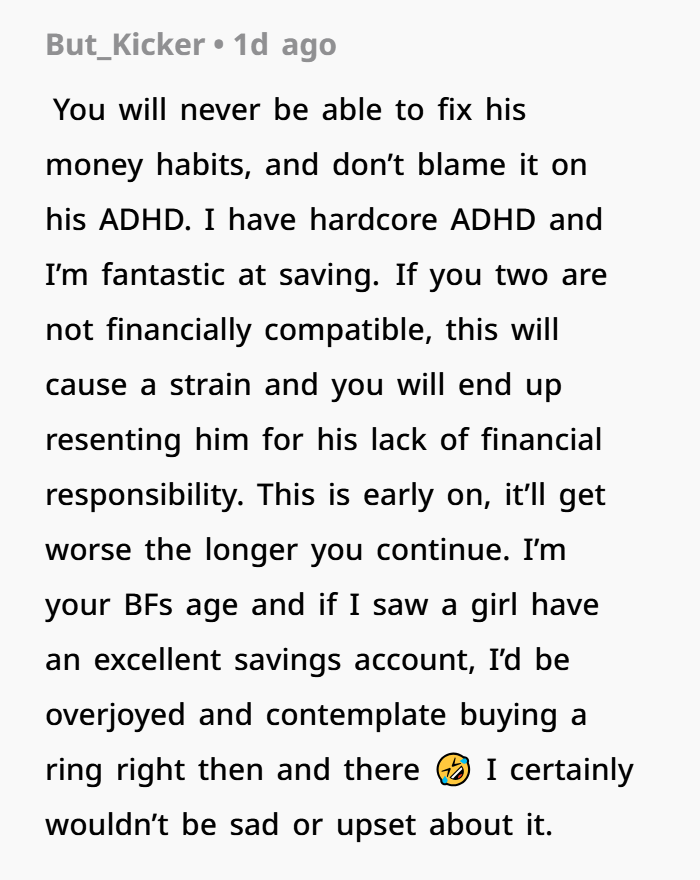

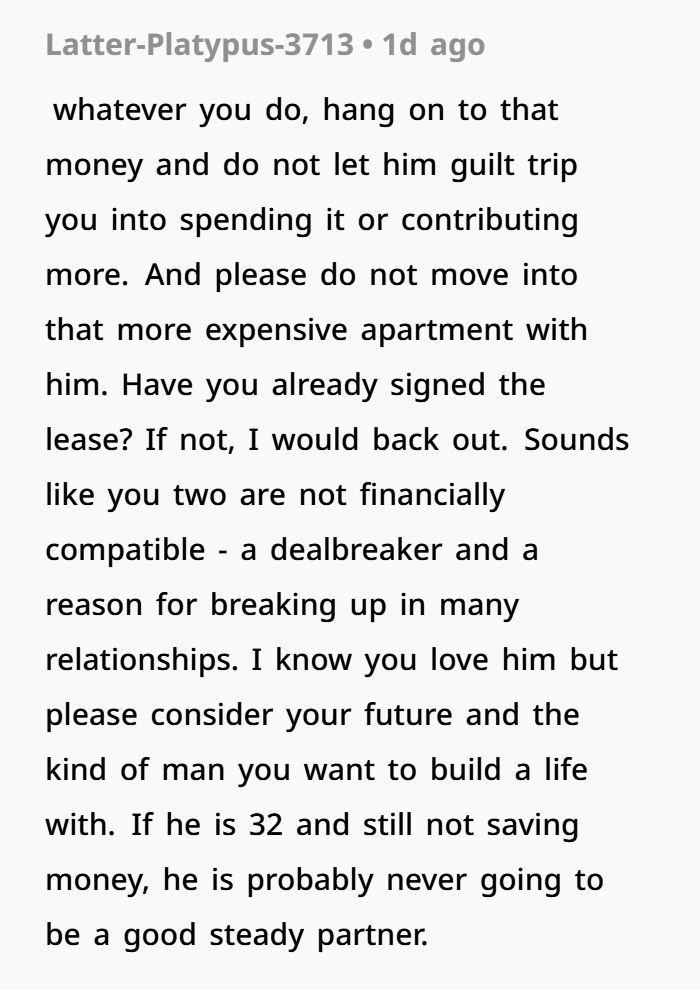

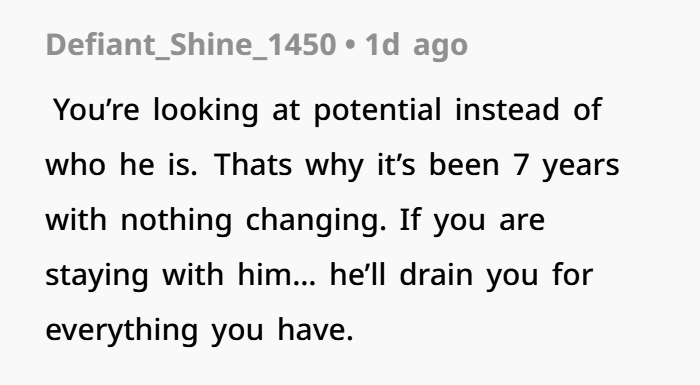

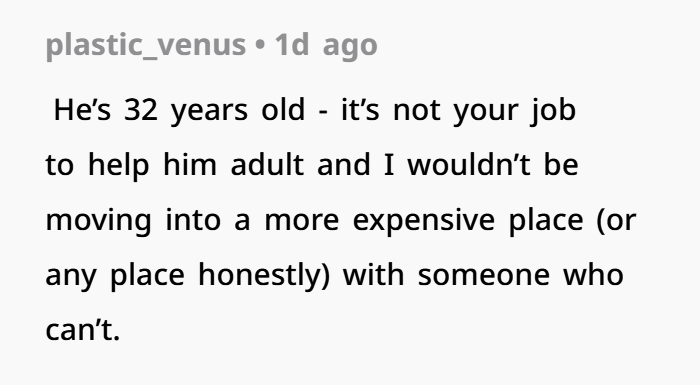

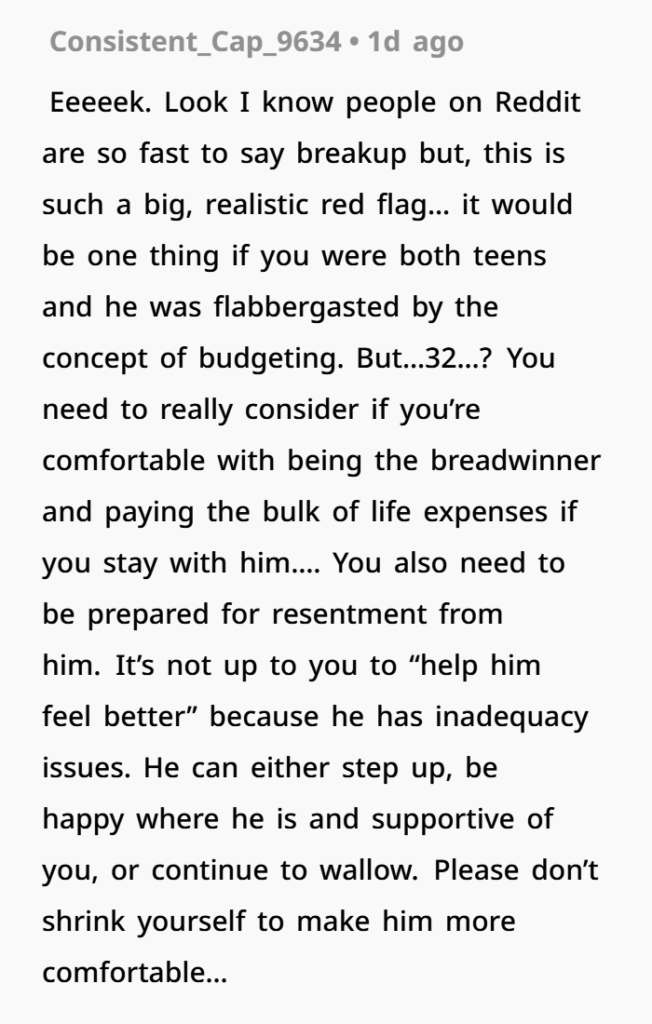

Readers had plenty of thoughts to share, and the woman replied to some of their comments along the way

Final Thoughts

This story is not just about savings or money.

It is about:

- Financial responsibility

- Relationship compatibility

- Mental health and ADHD

- Trust and stability

- Long-term life planning

In the end, love alone is not enough for a stable future. A strong relationship also needs financial responsibility, teamwork, and consistent habits from both partners.